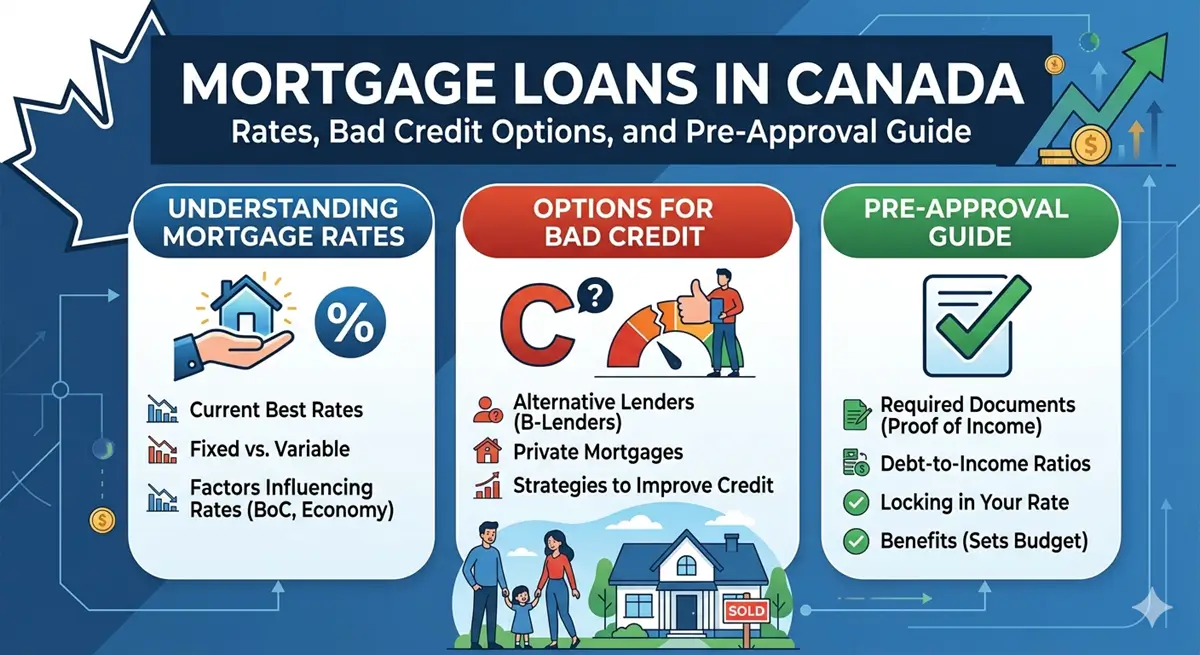

For many Canadians, buying a home is one of the biggest financial decisions they will ever make. Whether you are a first‑time buyer, upgrading your home, or refinancing, understanding how mortgage loans work is essential. This includes knowing how mortgage loan rates are determined, what options exist for mortgage loans with bad credit, and how to secure a mortgage loan pre‑approval that strengthens your buying power.

This guide breaks down everything Canadians need to know so you can move forward with confidence.

A mortgage loan is long‑term financing that allows Canadians to purchase property while paying it off over time. Your lender provides the funds upfront, and you repay the loan through scheduled payments that include both principal and interest.

Mortgage loans in Canada are influenced by several factors:

Because each borrower’s situation is unique, lenders evaluate risk differently — which is why understanding your options is so important.

One of the most common questions Canadians ask is whether it’s possible to get mortgage loans with bad credit. The short answer: yes, it’s possible — but the process works differently than it does for borrowers with strong credit.

| Score Range | Category |

|---|---|

| 760+ | Excellent |

| 725–759 | Very Good |

| 660–724 | Good |

| 560–659 | Fair |

| Below 560 | Poor / Bad Credit |

If your score is below 660, you may be considered a higher‑risk borrower. Check Your Credit Score Here for Free

These lenders specialize in helping borrowers who don’t qualify through traditional banks. They offer more flexible approval criteria but may charge higher rates.

B‑lenders are regulated financial institutions that work with borrowers who fall just outside bank requirements. They often accept lower credit scores, higher debt ratios, and non‑traditional income sources.

Private lenders focus primarily on the property’s value rather than your credit score. They are often used for short‑term financing or unique situations.

Understanding mortgage loan rates is essential because your interest rate directly affects your monthly payment and total cost of borrowing.

Your rate stays the same for the entire term. Best for Canadians who want stability and predictable payments.

Your rate fluctuates based on the lender’s prime rate. Best for borrowers comfortable with market changes and potential savings.

Your payment changes as the interest rate changes. Best for borrowers who want consistent principal repayment.

Before shopping for a home, getting a mortgage loan pre‑approval is one of the smartest moves you can make.

A pre‑approval is a lender’s written commitment stating how much they are willing to lend you, based on your income, credit score, debt levels, down payment, and employment history. It also typically includes a rate hold that protects you from rising mortgage loan rates for 60–120 days.

With so many options available, choosing the right mortgage loan can feel overwhelming. Here’s a simple framework to guide your decision:

Whether you’re exploring mortgage loans with bad credit, comparing mortgage loan rates, or preparing for mortgage loan pre‑approval, the Canadian mortgage landscape offers solutions for every type of borrower. For more tools, guides, and mortgage resources, visit MortgageLoansCanada.ca.

Yes. Many Canadians secure mortgage loans with bad credit through alternative lenders, B‑lenders, or private lenders. Requirements may differ, but approval is still possible.

Yes. Mortgage loan rates can change based on the Bank of Canada rate, bond yields, and lender competition. A pre‑approval can lock in your rate for 60–120 days.

A pre‑approval typically involves a hard credit check, which may cause a small, temporary dip in your score. This is normal and expected.

Most lenders can issue a mortgage loan pre‑approval within 24–72 hours once all documents are provided.

Not necessarily. While a larger down payment helps, many Canadians qualify with the minimum required amount, depending on the property price.